How to adapt to the agency sales model: A 4-step guide for car dealers

According to an exclusive investigation by Car Dealer Magazine1, 18 car makers have already switched or are planning to switch to agency sales in the UK, while only eight have ruled it out completely. The rest are either silent or undecided. Agency sales model is coming and aims to significantly change the business model and large part of operations of a typical car dealership. The profitability, among other parameters, is under attack here. So how can a dealership adapt and protect its business?

The agency sales model is a new way of selling cars that is gaining popularity among car manufacturers and consumers. In this model, the car manufacturer sells the car directly to the customer via its own website, and the dealer acts as an agent who delivers the car and provides after-sales service. The dealer receives a fixed fee from the manufacturer for each car sold, instead of earning a margin from the sale price.

The agency sales model has several advantages for both the manufacturer and the customer. For the manufacturer, it allows them to control the pricing, distribution, and marketing of their cars, as well as to collect valuable customer data. For the customer, it offers a transparent, hassle-free, and consistent buying experience across different channels and locations.

However, the agency sales model also poses some challenges and risks for car dealers, who have to adjust their operating model and strategy to survive and thrive in this new environment.

So how can car dealers adapt to the agency sales model and maintain their profitability and relevance? Here are some recommendations based on best practices and expert opinions:

-

Focus on customer service and retention

The agency sales model reduces the dealer’s role in the sales process, but increases their role in the service process. Therefore, dealers need to focus on providing excellent customer service and building long-term relationships with their customers. This can help them generate repeat business, referrals, and loyalty. Dealers can also offer value-added services such as maintenance packages, accessories, insurance, and financing options to increase their revenue streams.

-

Embrace digital transformation

The agency sales model requires dealers to adopt digital tools and platforms to communicate and interact with their customers and manufacturers. Dealers need to invest in online presence, e-commerce capabilities, CRM systems, and data analytics to enhance their efficiency, effectiveness, and customer satisfaction. Dealers can also leverage social media, online reviews, and content marketing to increase their brand awareness and reputation.

-

Collaborate with manufacturers

The agency sales model changes the relationship between dealers and manufacturers from adversarial (or at least cautious and tense) to collaborative. Dealers need to work closely with their manufacturers to align their goals, strategies, and operations. Dealers can also benefit from the manufacturers’ support and resources in terms of training, marketing, technology, and incentives. Dealers should also provide feedback and insights to their manufacturers to help them improve their products and services.

-

Diversify your portfolio

The agency sales model may limit the dealer’s ability to negotiate prices and discounts with their customers and manufacturers. Therefore, dealers need to diversify their portfolio of brands and products to cater to different customer segments and preferences. Dealers can also explore new opportunities in the used car market, which is expected to grow in demand and profitability in the era of transformation towards electromobility.

The agency sales model is not a threat but an opportunity for car dealers who are willing to adapt and innovate. By following these recommendations, car dealers can create a competitive edge and a sustainable future in the changing automotive landscape.

Do you want to help with the digital transformation of your sales, marketing and aftersales care? Our consultants are happy to discuss your current issues. Contact us!

The end of internal combustion engines will change the rules of the game

Internal combustion engines are nearing the end of their lives. In Europe, a deadline of 2035 has been set and, in the US, they have begun talking about a similar date to come into effect, which is already valid in California for example. But the end of internal combustion engines will change the car market in one fundamental way – it will remove the main barrier to entry for Chinese carmakers, and they cannot wait for this to happen.

Inconspicuous China is dominating the EV market

Anyone that knows at least a little about the Chinese car market knows that there are dozens of domestic carmakers that are literally fighting for a piece of the local market. And it’s not a small market. In 2010 it reached a million cars sold per month and just before the onset of the pandemic it was more than three million. The pandemic and ensuing global chip shortage pushed June sales to just over two million, a 28% drop from December 2020, but brought record sales of electric vehicles. They already account for 15% of all vehicles sold and their share is constantly growing (by 160% year-on-year). And Chinese carmakers are continuously pushing out new models. Even compared to the locally very well-established Tesla, the pace of production is breathtaking. At the same time the Chinese market represents 50% of the global EV market and McKinsey expects that by the year 2030, 9 million EVs will be sold in China yearly.

In the first half of the year, 1.1 million EVs were sold in China, while in other than the Tesla Model 3 and Model Y, the ranking of the top 10 best-selling brands was occupied exclusively by Chinese manufacturers. The Wuling Hong Guang MINI EV minivan is enjoying massive success, with an

incredible 181,810 units sold. The monthly sales of this mini-truck in China reach similar numbers as the European sales of the Volkswagen Golf. The top 10 is completed by BYD, Great Wall, GAC (GAIC), Li Xiang, Chang’an and Chery. BYD has been aggressively targeting Tesla, especially in recent months. However, Chinese carmakers are now chomping at the bit in other markets as well.

Why China is beating the US in electric vehicles

Inconspicuous expansion

The fact that the Chinese can gain significant traction is best shown on the Russian market. Russia does not have as strict emission limits as Europe or the US, so the Chinese can even compete with internal combustion engines. The Geely Group, the Chinese owner of Volvo and the 9.7% shareholder of the German Daimler, which last year founded a new EV brand called Zeekr to be launched this autumn, best shows how quickly the Chinese carmaker can succeed here. Geely only entered Russia last year, as part of its expansion out of China to markets in the Philippines, Kuwait, Saudia Arabia, and Myanmar. In Russia it offers the SUVs Atlas, Coolray, Tugella, and Atlas Pro. The latter, built on Volvo technology, climbed up to the ranks of the top 25 best-selling cars in Russia in June 2021, with sales increasing 300%. Coolray can be compared to the Škoda Karoq in terms of size, technology, and performance. In a price comparison, the Karoq starts at 14% more expensive for the base model, but is almost twice as expensive as a Geely when fully equipped. The Geely also comes with a 5-year warranty. Geely’s approach to the Russian market gives an idea of what such an expansion in the EV area might look like. The above mentioned Wuling Hong Guang MINI EV will cost only 4500 USD, a third less than the comparable Citroen Ami.

Western joint ventures in China will help the Chinese in the West

In fact, the expansion of the Chinese to the West may happen much faster than expected. The Chinese can benefit from their current joint ventures (e.g., SAIC Volkswagen, SAIC Volkswagen, SAIC GM, BAIC Hyundai, DPCA (Dongfeng and PSA), GAIC Toyota, GAIC Tesla, and many others), which Western carmakers had to establish as a condition of entry into the Chinese market. Additionally, the Chinese carmakers can benefit from their holdings in Western carmakers such as in the case of Geely or SAIC (GM, Roewe).

China took Norway by storm

The Chinese expansion into lucrative Western markets has already begun. The most lucrative market, Norway, where B/PHEV has reached an incredible 84.9% of total sales in July 2021 with 17,323 cars sold, has seen the entrance of the Chinese BYD with its family SUV Tang. BYD wants to sell 1500 of those vehicles this year and is already operating on Scandinavian markets with its electric buses. On one hand, entry to Norway is much easier than to other European markets, but on the other hand, it is the most competitive electric vehicle market in the world.

At the same time, BYD, as in China, will meet its match mainly with Tesla, who has nearly doubled the sales of the 2nd most popular electric car, the Ford Mustang Mach-E, with sales of the Model 3 in Norway. The target of 1500 cars sold in the first half of the year in Norway could be enough to place BYD in 10h place, which was occupied by the “British” MG ZS EV with 1579 cars sold. But it may be worth remembering that MG Motor was bought in 2005 by the Chinese Nanjing Automobile Group, a member of none other than SAIC, which is actually has a joint venture between VW and GM in China. In addition, the 9th place position with 2349 cars sold in Norway belongs to the Polestar 2 model, part of the Chinese Geely. So, in fact, Chinese electric cars have been quietly building a presence in the West for quite some time.

How to prepare for the Chinese? They are not afraid of new business models

Chinese carmakers have long understood that classic sales models are dead, or that they do not work so well with EVs. In addition to the classic model of owning a car or leasing, you will often come across a model for battery leasing in China. You can buy a car from the carmaker, but you will get its battery in the form of a service. Therefore, you don’t have to worry about its capacity decreasing, subsequent exchange, or disposal. The Chinese thus eliminate the biggest barrier to purchase, especially for cars with low battery capacity, which are logically cheaper.

In addition, some dealers have started offering another model – you own a vehicle without a batter, you are leasing a battery, but not a specific one. So, when you need to hit the road quickly, you just have the battery replace by a freshly recharged one and you’re driving. Naturally, such cars are built for this service so that the replacement only takes a few minutes. Carsharing is also very popular, which allows you to rent an EV for a specific number of minutes.

So how can you prepare for the expansion of the Chinese? It is important to know your customers and what they expect from their car. But you must also be prepared for the rapid introduction of new business models, which are so far unusual for Western carmakers. A specialized flexible cloud-based Automotive CRM for car dealers can help you with this, which will not only easily help you add new brands and models to your portfolio, but also introduce new sales and service models using all the existing information you have about your customers.

Sources

https://www.reuters.com/article/us-autos-emissions-california-exclusive-idUSKBN2BE111

https://tradingeconomics.com/china/total-vehicle-sales

https://insideevs.com/news/522274/china-plugin-car-sales-june2021/

http://global.geely.com/media-center/news/geely-auto-2020-sales-reach-1-32-million-units/

https://insideevs.com/news/517969/norway-plugin-car-sales-june2021/

Connected Cars

Connectivity in modern cars opens up a wide range of new possibilities. At the same time dealers can take advantage of these opportunities and create their own services. Where did connectivity in cars come from, what direction is it going, and how can money be made off of it?

From OnStar and eCall to OTA updates and beyond

Car connectivity dates back to 1996, when a subsidiary of General Motors, OnStar, began equipping selected group cars with a paid (subscription-based) system for emergency calls, and later for navigation and remote diagnostics. Three years later with the launch of the European satellite navigation project Galileo, an eCall system was proposed to automatically contact emergency services in the event of an accident (including the geographical location and condition of vehicle systems). The eCall system was to be implemented in all cars sold in the EU, however this did not happen until 2018. In the meantime, not only did systems for location tracking and remote diagnostics get into cars, but thanks to Tesla also remote updates for various functions, including the possibility of unlocking speed boosts (Ludicrous mode) or increasing battery capacity (in the Model S for example where the lower-end model has the same battery as the high-end car). Today, connectivity in cars, usually provided over a mobile 4G network, can provide support in emergencies, fleet management, and diagnostics. However, it also allows carmakers and dealers to sell new functions and benefit from marketing collaboration, for example when recommending new applications or points of interest on a journey.

Connectivity brings new applications

However, connectivity in cars will soon go much further. Soon we will see the remote prediction of a failure, which is commonly seen today for example in elevators or on production lines, which will help identify potential problems in the car over time. There are also new applications for leasing companies, company fleets, and dealerships that can work with existing telemetry data. Monitoring a car’s daily mileage limit, or even the departure from the rental region is child’s play, even today.

The future lies in infrastructure, security and autonomous management

The key is however, future connectivity, which is moving in a completely different direction. For example, pilot projects are funning to connect cars to parking lots so that drivers will know which lots have a free parking space. Since the time of RDS-TMC, traffic intelligence and route rescheduling through navigation have become a standard practice. In the near future however, it will all be controlled by artificial intelligence, which will aim to proactively optimize road traffic permeability to prevent traffic jams.

The breakthrough will occur after the introduction of inter-vehicle communication. Thanks to data from cameras and other sensors, cars will be able to automatically inform each other about obstacles or animals on the road, ice, weather conditions, or even pedestrians. And the driver, but later even the vehicle itself, will be able to react in real-time, which will help prevent accidents.

What will connectivity bring to dealers?

The main question for car dealers is different – how to make money on it all? And the possibilities are perhaps unexpectedly wide. The first, most logical, possibility is to reduce fleet management costs. Today it is no longer a problem to remotely monitor all replacement and test vehicles, both in terms of their location and use, but also for example to check tire pressure, batter condition (including the EV powertrain), fuel levels in the gas tank (which is especially useful for diesels), error codes, or whether the car has been parked somewhere for a long-time while unlocked. This, of course, will help prevent a number of problems.

But there is another option – if you have cars in the fleet, from which you can read even the driving style and the way the car is used, it can dramatically help you with sales, including upsell accessories. Do you have a customer who plays loud music in a loaner car? How about offering him/her better-quality speakers in his vehicle? Do you have a customer who has rented a more powerful car than he/she current drives and enjoys fast acceleration and higher speeds? How about offering an inventory car with higher performance? Do you have a customer that travels mainly short routes around the city? How about offering him/her an EV? There are many possibilities, you just need to have in addition to car connectivity, a 360° customer view – to know what kind of car/s they have, what is important to them, what cars they bought in the past, what they complained about, etc. Konica Minolta’s specialized Automotive CRM will help you with exactly that.

But that’s still not all. Do you already have someone who checks the status of your dealer fleet by measuring data remotely? What about offering your customers a paid remote care service for their car? Covering the same things you do in your fleet – tire pressure, oil level, battery status, error codes (including e.g., a broken bulb), unlocking/locking the car. It is then super easy to pick up the phone and call a customer about a problem with their car when it is automatically detected. Just don’t do it for free.

In the future, connected cars will bring even more business

But that’s still not all, because there will be other business opportunities in the future. A number of carmakers, including Mercedes, are preparing their dealers to sell features online. It is about far more than just navigation, which has long been the primary sold feature by dealers. Dealers will now be able to sell a range of new features, and if they know their customers and their needs well, they will be much more successful than carmakers in selling these features. In addition, as the complexity of new features increases, so will the need to train customers in their use. And this is another opportunity that many dealers are already taking advantage of. In the future, it will no longer be about defensive driving schools, but also about teaching how to use driving assistants or built-in infotainment. Dealers who have a 360° customer view will significantly expand their chances of earning money from these opportunities.

Sources:

https://open.spotify.com/episode/4UmbmclpLnDcbb766aGNKY?si=NRa7eK3lTUGEN-1hPVrOmQ&dl_branch=1

https://en.wikipedia.org/wiki/OnStar

https://en.wikipedia.org/wiki/ECall

End of combustion engines in the EU by 2035?

In mid-July, the European Commission decided that it wanted to the end the sale of motor vehicles with internal combustion engines by 2035 to be replaced by electric vehicles. This step comes at a time when a significant number of car manufacturers have announced the end of internal combustion engines in horizon of the next 15 years. What does this mean for dealers?

The EU intends to increase emission standards

The European Union is failing to meet its original targets for reducing CO2 emissions not only from car transport. With weather fluctuations in July causing large-scale floods in Belgium, Germany, and the Netherlands, a tornado in the Czech Republic, or an unexpected heat wave in Spain, the climate change debate is intensifying. According to commissioner Adina Valean, transport is responsible for 29% of all EU greenhouse gas emissions (cars are responsible for 12%). By 2050, the commission wants to reduce these emissions by 90%. Banning internal combustion engines in cars and vans could be a way to reach that goal.

Some manufacturers are in turmoil

At present, it is still only a proposal that is opposed not only by some representatives of the car industry, but also by politicians. For example, the German MEP Peter Liese said that the end of internal combustion engines by 2035 could be a major problem for manufacturers of components of these engines. At the same time, he is not the only one in the European Parliament who has reservations about the current proposal. So, what will happen next?

Every two years, a report on the direction of the market is drawn up, and a complete revision of the regulation is due in 2028. At present, cars in the EU can produce 95 g of CO2/km, while in 2030 it should be 55% of that figure and from 2035 net zero. For delivery vans, it is now 147 g of CO2/km, which will fall to half by 2030 and by 2035 should also be zero. Until 2030, only small manufacturers with an annual production of 1000 – 10,000 cars or 22,000 vans can apply for an exemption. The European Commission has already announced that it will prepare proposals for the sale of electric cars, which will come into effect by 2030 latest. Similar programs already exist in key markets such as France or Germany, contributing to a massive increase in electric car sales.

Electric cars lack infrastructure

The key problem, which has been highlighted by manufacturers, is the lack of charging infrastructure. Some car manufacturers have strongly criticized the European Commission for this, suggesting that if the EU does not invest in charging infrastructure, it is unrealistic to achieve the newly set goal. The European Commision responded by proposing mandatory construction of public charging stations (paid for with public money) on all major roads with a maximum distance of 60 km between them by 2025. By 2030, there will be total of 3.5 million public charging stations in the EU, and 16.3 million by 2050. However, the charging stations are being built in parallel by the manufacturers themselves, whether it is Tesla or the Ionity consortium backed by BMW, Ford, Hyundai, Mercedes-Benz, Volkswagen, Audi, and Porsche.

Dealers and service stations are not ready for electric cars

The electric vehicle problem will soon affect dealers as well. Although they are ready to sell electric cars, their infrastructure is absolutely not adapted for them. In short, dealerships are not ready to recharge 15 demonstration vehicles at the same time with fast charging, not to mention recharging vehicles in service. Building a charging infrastructure consumes money and time. In addition, many dealers will struggle with the insufficient capacity of the electrical transmission grid, as even 10 fast charging stations with an output of 150 kW will require an electrical connection of a respectable 1.8 MW, which is equivalent to the electrical consumption of a medium-sized factory. The European Union will fact the same problem. To be able to transition to electric cars, it will be necessary to significantly strengthen the transmission grid and electricity generation capacity.

Another problem will be with service. New tools will be needed for the repair and maintenance of electric cars as well as different facilities. This will apply in particular to the handling of batteries that are highly flammable, explosive, susceptible to physical damage, and most importantly, high weight. While portable systems for removing an internal combustion engine have been part of the standard equipment of a car service for decades, most services do not have the equipment or the necessary space for handling batteries.

Prepare for the revolution in time

The necessary preparations for dealerships and service centers could thus be divided into three categories. The first is the charging infrastructure, not to mention that some discounted charging point for customers could be an interesting marketing tool. The second category is service and facilities. Both will require massive investments and major renovations with long-term returns. The third category is sales. This will change significantly, because customers will suddenly become interested in a completely different range of parameters than before – range, charging speed, availability of charging stations in their place of residence, speed of single-phase charging (from 230V home chargers), etc. A tool that can deal with these changes is the specialized Automotive CRM from Konica Minolta, for example. It enables a comprehensive 360 ° customer view, from their interactions with car dealers and service centers, thanks to which you will more easily identify a suitable electric car for them. Furthermore, you can combine your offer with targeted subsidy incentives that the EU is now preparing with member states. As always, the player that wins is the one that is able to adapt the fastest to market changes.

Sources

https://fortune.com/2021/07/14/automakers-europe-ban-of-new-combustion-engine-cars-by-2035/

How carsharing affects your business

Carsharing is an emerging trend, heading to all major cities across developed countries. What does carsharing look like, what can we expect from it, and how will it change the car business?

What is carsharing?

Carsharing is a relatively new approach to car use based on the idea of sharing one car with multiple people. Standing behind the idea is the rather logical reasoning that suggests that for most of the time we own a car, it sits in the garage. Therefore, car ownership is relatively inefficient with high fixed costs – acquisition costs, road and environmental taxes, leading to a high cost per km driven. The idea of carsharing at the turn of the century aimed to reduce these costs.

However, other, newer factors are increasingly supporting the idea of carsharing. Firstly, cities are becoming more and more crowded and finding a parking place is becoming more difficult. Carsharing solves this problem because it reduces the number of cars per capita. Secondly, too many cars is unecological as each car produces a significant carbon footprint during production, transport, and disposal. The is doubly true for electric cars because the lithium ion batteries often need to be mined and manufactured in areas far away from vehicle production. Additionally, these batteries are difficult to dispose of in an environmentally friendly manner. It therefore makes sense to reduce the volume of cars produced. It therefore makes sense for governments to support carsharing among cars with minimal (e.g., CNG) or zero emissions. The bottom line is thanks to all these factors, carsharing is riding on a wave of popularity.

Carsharing is always different

There are several types of carsharing. They all build on the one main idea that you do not actually use or need a car most of the time. Depending on the type of carsharing, various other factors come into play. In particular, the following three carsharing models are most popular worldwide:

- Co-ownership – literally the joint purchase of a car by several households or a community, but with not for professional use.

- Professional carsharing (free-floating) – built on vehicles purchased by a carsharing operator (often associated with a car manufacturer, importer, or dealer). The goal is to profit from very short-term (often hours or even minutes) rentals inside large cities. Government support often plays a role in the form of free entry to the city center, free parking, or relief from road taxes and tolls. This usually comes with a requirement for low-emission and zero-emission cars.

- Carsharing built on a shared economy (peer-to-peer) – essentially an AirBnB for cars, where people or even companies share their privately owned cars with others. The carsharing provider merely provides a platform for carsharing.

In the last two types of carsharing usually work where those interested in taking part register on a carsharing platform, provide necessary documents, enter their payment card details, and if necessary, make a deposit or pay a recurring monthly fee for using the platform. They then access a mobile application that shows them available cars in their vicinity. Payment is made for the duration of the loan (usually in minutes), for kilometers travelled, or a combination of both. Many carsharing plaforms offer discount packages for a fixed amount of time – certain hours, days, weekends, weeks, etc.

Professional carsharing services offer the possibility of using a chip card or mobile phone instead of a key in modern cars. Carsharing users only need to walk up to the parked car on the street, activate the car via the mobile application, and then they can immediately unlock it and drive away. This solves the problem of securing and sharing car keys. Refueling is usually solved through refueling cards or access to charging points. The carsharing operator then continually maintains the entire fleet including service intervals, changing tires, and, if necessary, settling insurance claims or redistributing cars to different locations.

Autonomous cars will change the rules of the game

Another form of carsharing will appear very soon. General Motor’s subsidiary, Cruise, has been working on something new for several years in cooperation with Microsoft. Cruise is taking advantage of fully autonomous electric Chevrolet Bolt EV vehicles. The first active test took place in October 2020 in San Francisco. In reality, it was the result of five years of research and development, where electric Bolts had traveled autonomously for more than 2 million miles.

GM’s Cruise is more of competition to Uber, however. From the user’s point of view, it works identically. The user opens the Cruise application on their mobile phone, orders an autonomous Bolt EV to their address, enters the destination address, and that’s all there is to it. The Bolt EV, which can be followed in real time in the application, will come for the client, take them to a destination, and then automatically go pickup another client. The user is then charged for the driving duration, similar to many carsharing programs, and the same as with Uber. It is important to note that perhaps it is not an accident that the public test of Cruise took place during the coronavirus pandemic. COVID has significantly changed views about the possibility of driverless passenger car transport, and mass public transport has suddenly become dangerous.

What carsharing means for auto dealers

At first glance, it might seem like carsharing is something that is anti-sales. The goal is for one car to be shared among many people. But in the days of coronavirus, carsharing can be a way to attract more people to personal cars. Even a person without their own car can get to work for a few dollars or Euros, safely, and without being in contact with other people.

Apparently, car manufacturers also see an opportunity for growth in carsharing. And we don’t just mean GM and their future attempt at creating competition for Uber. Some car companies are working on their own carsharing programs. It is worth mentioning that Škoda Auto, part of the Volkswagen Group, has built its own carsharing program, HoppyGo, in several countries based on an open economy. It is used to share cars from any brand.

Professional carsharing services are actually a classic fleet customer, which, unlike large companies, has the potential to sell, for example, a pickup service, car cleaning, sales or rental of accessories, etc. Everything is about how dealers integrate carsharing, because stopping it is not an option.

Sources

https://en.wikipedia.org/wiki/Carsharing

A car subscription added to operational leasing

A new car every month. A car subscription is exactly what some car manufacturers and leasing companies are offering in selected countries. This relatively new service is intended to complement increasingly popular operational leasing and could quite possibly shake up the car market. What will be the impact?

What is a car subscription?

A car subscription is a kind of intermediate stage between a rental company and a traditional operational lease. As with a car rental company, the customer does not need to worry about anything – service intervals, tire changes, insurance, road and environmental taxes, and in the case of electric or hydrogen cars, sometimes even charging is included in the service. The user only has to take care of refueling, windscreen washer fluid, tolls, and parking fees, nothing more – in short, a car as a service. Many subscription services even include delivery of the car to an agreed address.

The key here is the duration of the subscription – it ranges from a single month to a quarter, half year, nine months, or a year. Sometimes, for example with Porsche USA, it is possible to rent a car for a single day. Car subscriptions are offered in various markets either directly through car manufacturers, leasing companies, or rental car companies. It is a special market where all these players compete at the same level. After the end of the several-month contract, it is possible to continue with a new car or terminate the contract.

Subscription vs. leasing

At first glance, the differences between a subscription and leasing may not be obvious. The main difference is the duration of the contract. The second difference is that opposed to a regular lease, it is not possible to buy the car at the end of the contract, like a car rental service. A key difference compared to operational leasing is that car does not have to be new and that it is not possible to choose its configuration. Most offers include cars that are up to two years old and a pre-selection of models, engines, and equipment.

The truth is that current operational lease offers are sometimes very similar to subscriptions. There are leasing providers that offer only annual or even six-month contracts, and in addition to insurance and taxes (road and environmental), they include tire rotations and service in the lease. These offers are not available in all markets, and they are also not always welcomed with open arms. Car subscriptions can also be attractive from a marketing point of view. In the days of Spotify, Netflix, Adobe Creative Cloud, and Microsoft Office 365, more and more companies and consumers are getting used to everything in subscription form. In many markets there are even mobile phone or laptop subscriptions. So why not “sell” and especially promote cars in the same way?

Who will benefit from a subscription?

A subscription would be ideal for new drivers. Of course, most providers know this, and that’s what they’re trying to prevent. Many services require a minimum age of 25 and several years of driving experience. So, for new drivers, the service is, so far mostly unavailable.

However, there are other usage scenarios for the retail segment. A family car for a few months is suitable for employees who have been recently fired and need to return their company car, or for those who take a so-called sabbatical for exactly six months or a year. In some countries, the possibility to cover the absence of a company car applies to a large group of customers who would welcome such an offer with open arms.

Car enthusiasts might enjoy another option with brands such as Porsche. Having a new, and especially different Porsche every month is a childhood dream of many boys. But few can afford it. At $3100 a month plus tax, which is the price of Porsche Drive in several major cities on the West Coast of the United States, such a dream becomes a reality, if only for a few months.

The ideal target group is also companies, especially those running a seasonal business. With limited contracts, they can rent company cars only for a few months, for example during a given season. However, it could also be advantageous for companies employing interns or employees from other branches. Another interesting target group could be contractors who are in a location for only a few months before they finish their contract.

And then we have an electric car subscription. For many companies they serve as a demonstration of the company’s commitment to the environment. And being able to show purely electric cars at summer company events for example, is something that many companies would be interested in. After all, Citroën chose to cooperate with selected companies to offer its utility vehicle, Ami, as a subscription. And other manufacturers such as Mercedes-Benz or Ford have also begun to offer a subscription service for their commercial vehicles.

Car subscriptions are gaining traction

But do car subscriptions have a chance to gain traction in the market? Definitely yes. It just may not be a widely available service. They can be expected to address only specific segments and parts of the market. However, as you will not find them everywhere in the US, the same is true for Europe. But how will car subscriptions change the market?

Some automakers want to go the way of direct sales or sales through their own financial institutions. Of course, this will not please dealers much, especially if the pricing policy will be more favorable then buying your own car. But carmakers will not be able to service the cars themselves. Dealers will be needed for this. For dealers, it pays to cooperate with car manufacturers. Those who are more proactive will have an advantage. This will especially apply to larger dealerships with multiple locations.

Those who have solid CRM data and know their clients will have a better bargaining position for car subscriptions, not only in cooperation with manufacturers. Dealers using advanced specialized CRM systems such as Automotive CRM, which offers a 360° customer view including social network interactions, will be able to generate quality leads for subscription services.

In addition, dealerships will be paid a handsome fee for providing quality leads, just as they do today with leases and loans. At the same time, winning a customer if only through a commission on the car subscription and service can be a source of new income. After all, it can be expected that car subscriptions will be purchased by different customers than those who typically come to buy a new car. And how are you prepared to take advantage of the opportunity that car subscriptions bring?

Sources

https://www.forbes.com/wheels/advice/car-subscription-services/

https://www.thebalance.com/best-car-subscription-services-5095656

The Model 3 is making an attack on Europe with electric cars

JATO has published its report on car sales in the EEA markets for Q1 2021. It is full of surprises. The Tesla Model 3 became the fourth best-selling European car, and the volume of new registrations was the second worst since 1986. Sales of diesel and gasoline engines are in significant decline.

Compared to last year, the market is growing, but it is still a miserable situation

In the European Economic Area, 1,374,313 passenger cars were newly registered in the first quarter. Compared to March 2020, this is a significant increase of 63% and yet it was the second worst first quarter since 1986. The decline of the car market to 35-year-old levels is painful for dealers as well as manufacturers. But not all of them. The radical declines in sales, together with emission regulations on cars with internal combustion engines means the time is ripe for electric cars.

Electric cars are on the rise while diesel and gasoline are slowly losing popularity

Electric car sales are skyrocketing. While in 2019 they accounted for only 4% of sales, a year later it was already 10%, and this year even 16%. In the context of total volumes, however, it is not so much growth as the collapse of the market. Nevertheless, taking a view of share of cars sold by type of drivetrain is interesting. Over two years, diesels fell from 32% to 24%, while gasoline fell from 64% to 58%. Electric cars thus ate more into the share of diesel cars, which is partially due to hybrids, which, after all, are more often combined with gasoline engines (even Volvo, who initially tried to combine diesel with electric).

Tesla Model 3 is the 4th best-selling car in Europe

What is worth mentioning is the rapid increase of Model 3 sales in Europe. With 23,755 new registrations, it placed in-between the Opel/Vauxhall Corsa and the Toyota Yaris. Only 2510 more registrations and it would have beat the Golf. It can also be assumed that those sales figures were not achieved due to lack of demand, but rather lack of Tesla production capacity. Year-on-year, Model 3 registrations increased by 52%, while the Golf saw a 43% decrease. Apart from the Model 3, the sales of only one car in the top 10 grew. This was the Peugeot 2008 with a 12% increase.

The Model 3 has become the best-selling model in the United Kingdom, France, Norway, Italy, Austria, Sweden, Switzerland, The Netherlands, Denmark, Portugal, Poland, Greece, Croatia, and, not surprisingly, Germany. However, in many of these countries there are incentives to buy an electric car as well as some other benefits such as free parking, toll exemptions, or free entry to city centers.

However, plug-in hybrids are also supported in some countries. It is therefore not surprising that all models in the top ten best-selling PHEVs enjoyed rapid growth in sales. BMW recorded the largest increases for the X1 (585% growth) and the 3-series (454% growth), followed by Volvo with the XC60 (427% growth), and the XC40 (402% growth).

European electric cars are playing second fiddle, at least for now

The rapid growth was also experienced by fully electric cars. It just wasn’t as strong. The Hyundai Kona (+228%), Peugeot 208 (+189%), and the Volkswagen Up (+187%) recorded the highest year-on-year growth. However, as much as the sales of European electric cars are growing, it is nowhere near enough to catch the competition. The American Model 3 sold more cars in Q1 in Europe than the Renault Zoe (3rd place), Volkswagen’s ID.3 (4th place), ID.4 (5th place), and Up (7th place), and Peugeot 208 (9th place) combined.

The electric offensive from the largest European and second largest global carmaker, Volkswagen, could hardly compete with another non-European player, Korean Hyundai/Kia. Within Europe’s best-selling electric cars, Hyundai/Kia have two participants – Hyundai Kona (5650 registrations and 2nd place) and the Kia Niro (4037 registrations and 8th place). In addition, another non-European carmaker, Nissan, with the Leaf (4503 registrations) made it into the top 10.

European carmakers have long lagged behind in electromobility. The only exception was Renault in cooperation with Nissan. On the other hand, the Volkswagen ID.3 and ID.4 bring significant innovation and their sales are not bad at all. It will therefore be interesting to see if and how quickly European carmakers regain dominance of the European market. The European-American Stellantis might make a splash. It holds only the last two places in the top 10 with the Peugeot 208 and the new electric Fiat 500. But more news is coming, and the ultra-compact Citroën Ami could gain traction very quickly in many cities and the island regions. After all, at home in France, you can buy it for as little as 3 408 € + 19,99 € monthly or for 7 390 €!

Source:

Stellantis – a new no. 4 on the car market is born.

In January 2021, the world’s number 8 and number 9 carmakers in terms of production merged into the Stellantis concern. With its joint production it will overtake General Motors and nip at the heels of the 3rd largest carmaker, the Renault-Nissan-Mitsubishi alliance, which holds the lead mainly in the area of electromobility. What will the combination of FCA and PSA bring? And will all of its 15 brands survive?

What will you find in the Stellantis porfolio?

A relatively wide range of car brands can be found in the Stellantis Group portfolio. The Italian classics Alfa Romeo, Maserati, the fading Lancia and the sports version of Fiat – Abarth are the luxury brands represented. The French are adding an emergency luxury offshoot of the Citroën DS, which is already beginning to bloom as an increasingly distinctive and independent product portfolio, similarly to Genesis and Hyundai.

Mainstream brands are also represented here – American classics like Chrysler, Dodge, its spin-off and now iconic RAM brand, and also Jeep, which was the only one that managed to gain a foothold in Europe. From originally German-British-Australian origin, we have Opel and Vauxhaul, from Italy we have Fiat, while the French add Peugeot and Citroën. Similarly to how American carmakers have struggled to gain a foothold in Europe, European carmakers have trouble breaking into the US and Canadian markets. But the same does not apply for the rest of American continent.

Commercial vehicles are also included. Peugeot, Citroën, as well as the Italian Fiat Professional have producing them for decades. The latter, thanks to cooperation with FCA, has been supplying vehicles to the American market under the Ram Trucks brand.

Finally, the latest piece of the puzzle is Mopar, originally a division of Chrysler, which provides spare parts, service, and customer care for Chrysler’s portfolio brands – Chrysler, Dodge, Jeep, Ram Trucks, and formerly Plymouth, Imperial, and DeSoto. Mopar will occasionally offer special editions of these brands, most recently the 2017 Mopar Dodge Challenger.

Savings and synergies

The merger of FCA and PSA into a single group, Stellantis, will bring what every merger should bring – savings and synergies. The expected savings is already known in advance even though all factories will remain open and at current production. Stellantis is expected to save 6 billion dollars a year. From where will Stellantis realize these savings?

First and foremost, sharing modular platforms and drivetrains, as the VW Group has been doing very successfully for many years. The problem is that the North American and European requirements for NOx and CO2 emissions are not exactly compatible. This is especially the case for a number of Japanese carmakers, especially in Europe, and several European carmakers in the US. However, even if we omit the very complicated scenarios, the upside for Fiat and PSA in Europe will be significant.

Sharing the costs of developing electric cars and hybrids, including batteries, charging stations, environmentally friendly disposal, etc., is an extremely important point. As Renault-Nissan-Mitsubishi has shown, you must have scale for electromobility to work. Although Tesla has long been the synonym for electric cars, it does not make much money on them. The Franco-Japanese alliance is doing better. It manages to hold the number one position in sales of electric cars while maintaining profitability.

Savings in marketing and sales can also be expected. If Stellantis takes the VW route, as Mopar or Chrysler in the US did, and not the approach of Hyundai/Kia and earlier PSA, then it can very easily happen that joint multi-brand dealerships and service centers will appear. Moreover, as brands begin to share more key components, it’s a logical approach. For dealers and service provides, however, this will often mean the need to purchase new CRM systems that can handle more brands and share data across different company applications, marketing, and DMS. Automotive CRM from Konica Minolta is such as system, which also offers a 360° customer view across brands.

How to deal with brand cannibalization

Stellantis, unlike VW, has very elegantly stratified its portfolio of passenger car brands. Just like Chrysler, by itself, has gone the way of model diversification and individual specialized brands with Jeep, Ram Trucks, and Dodge offering distinct products. Fiat was also able to elegantly differentiate with Fiat, Lancia, Alfa Romeo, and Maserati offering little overlap between the brands. PSA was worse in this respect, but Citroën and Peugeot were able to differentiate in design and some of the specialties that Citroën kept for themselves. PSA as well as Opel/Vauxhall were then able to target a completely different market segment than Fiat and their brands.

The only areas time when it gets a bit muddy for FCA and PSA, more precisely for Fiat and PSA, is in commercial vehicles. But here they can take advantage of economies of scales. This may be particularly useful to Stellantis in the situation where the main rival of PSA, Renault, is toying with the idea of extending cooperation with Daimler in the area of commercial vehicles.

Overall, however, Stallantis has a great chance of avoiding the problems facing VW, where, for example, the Volkswagen Passat and Škoda Superb are fighting for de facto identical customers, while both brands are also pulling customers away from the sister Audi A4. Nevertheless, it is likely that Stellantis’ product porfolio will narrow. After all, the number of new models from Lancia, Alfa Romeo, Abarth or Fiat is not too large.

Strengthening in Americas and Europe, expansion in Asia and Africa

However, the Stellantis group does not plan to only save. On the contrary, it wants to jointly attack markets where it is not yet doing well. Namely Asia (mainly China and the Middle East) and Africa. Already the current product portfolio has something to offer for all three of these regions. For the Middle East, for example, Ram Trucks and Jeep are not in a bad position at all. The potential multi-brand dealerships will be able to choose the brands best suited for each region.

It is thus possible that in Africa or the Middle East, we may see Stellantis dealerships exclusively for 4x4s – from the cheapest Peugeot, Citroën and Opel cars, through utility Ram Trucks, more off-road oriented Jeeps, and luxury SUVs from DS, Maserati, or Alfa Romeo. It is also worth noting that Stellantis plays a relevant role in the minivan/MPV category, which are still sought after in Asia. There, the combination of large American MPVs from Chrysler and Dodge with smaller European MPVs from Citroën, Peugeot or Opel could be a big hit. Let’s let them surprise us.

Sources

https://www.wheels.ca/top-ten/these-are-ten-biggest-automakers-in-the-world/

https://www.carscoops.com/2020/06/renault-boss-keen-on-rekindling-partnership-with-daimler/

2030: Electric Odyssey – Electricity Is Changing the Way Cars Are Sold

More and more brands are moving towards complete electrification. Volkswagen, Ford Europe, Jaguar, Volvo, General Motors, and soon other carmakers will soon likely switch to electricity. Jaguar will be the first to do so by 2025, and most of the others will do so by 2030, with General Motors coming in last by 2035. However, with the change of propulsion, the business model will also change. What will this change mean for dealerships?

Say goodbye to internal combustion engines

Volkswagen will no longer develop new internal combustion engines, and the existing ones will ride out the era. At the beginning of March, this news unsettled the share price of the 2nd largest carmaker, but in a positive direction. During March, the share price jumped by an incredible 34.3%. By 2030, 70% of VW brand cars sold in Europe will be electric. In China and the US, it will be half that. By 2025, the carmaker will invest 16 billion Euros in e-mobility, hybridization, and the digitization of its cars. Autonomous driving should arrive by 2030.

Volkswagen is far from the only manufacturer to follow this trend. In January this year, General Motors announced the full electrification of all passenger cars, trucks, and SUVs. They came with his announcement just a day after the new American president returned to the fight against climate change. However, car manufacturers have other motivations for electricity. Jaguar Land Rover, which will convert its Jaguar brand by 2025 and the Land Rover brand by 2030, is looking for additional reliability that comes with electric power. The carmaker has been battling with reliability for a long time, and with electricity, it might finally have a way to get rid of the “unreliable” label.

Volvo will switch to a new sales model, and they’re not alone

Volvo, which in parallel has already launched its fully electric brand Polestar, that deals with certain childhood illnesses, has also opted for electricity from 2030. However, the propulsion system is not the only thing that will change. The carmaker plans to start selling all of its cars directly and online, similar to Tesla. From 2030, it will “sell” its cars in the form of a fixed monthly fee, including all service, insurance, and assistance services. This business model has long been used by Toyota worldwide for its Mirai hydrogen vehicles. However, Volvo and Toyota are not the only carmakers to toy with this business model. Many car manufacturers, most notably Volkswagen, play a key role in the area of finance, specifically of course, operational leasing. A car in the form of a service is popular in more and more countries around the world.

Direct sales from car companies will also radically change the dealer’s business model. They will continue to earn money from the service of these cars, perhaps much more than before because this business model will de facto end non-branded services. But then again, they will lose some of the commission from car sales. However, they may be able to sell different “things,” and we do not mean only accessories.

What does “digitization” mean?

As we said above, part of the 16 billion EUR that Volkswagen will invest over the next four years will go to digitization. This trend is also being followed by other car manufacturers such as Daimler (Mercedes-Benz) and BMW. But what does digitization mean? The idea is simple and again it is partly inspired by Tesla. As early as 2019, Mercedes-Benz stated that it wanted to earn from the sale of additional services and functionalities through its new MBUX on-board system platform. Initially, it started selling features such as Digital Radio, Apple CarPlay/Android Auto, and on-board navigation. In the future there should be many more features on offer. The car comes with all the features, which makes it cheaper to manufacturer at scale, and then they are only activated remotely.

A major breakthrough in distance-selling digital services will be autonomous control, which VW for example, has promised from 2030. There will be many more digital services, perhaps those we cannot imagine at the moment, and which will be location dependent. Today, we can mention for example, an overview of free parking spaces, or even automatic payments for parking, which are features that carmakers are currently testing in some German and American cities.

Of course, all these services will be sold directly by the carmakers. The transition to on-board systems with over-the-air updates will allow them to do so without any problems. But what carmakers cannot always do directly is sell the SIM cards that the cars need for connectivity. In addition, some customers will need help with the installation of some services, and that is something the carmaker will not be able to help with directly. It can easily happen that dealers will also perform the role of “user support” and training, as was once the case with computers, and later with mobile phones. Additionally, there may be potential for the sale of telecommunications services.

Will dealers also sell electricity?

Electrification brings another key element that not only automakers will have to tackle, and that is recharging. At the beginning Tesla incorporated a dumping policy, offering electricity at its own network of Tesla Supercharger stations to its car owners free of charge. Later, however, they started selling Supercharger access. Other carmakers are also building their own charging networks, usually in consortiums. The most important of these is IONITY, which currently brings together BMW, Ford, Hyundai, Mercedes-Benz, Volkswagen, Audi a Porsche. But most charging takes place locally, at a customer’s home or work, where the car is parked for many hours at a time and can be recharged in a slower and more battery-friendly way. However, customers then need to purchase the electricity from someone. In the European Union from an energy trader as European regulation has unbundled the electricity business into separate services of production, distribution, and sales to end customers.

At the same time, the electric car will need much more electricity and thus possibly a different supplier or tariff from the home or business. And within the sale of electricity are similarly high commission as in the sales of loans or insurance. This is a great opportunity for dealers, because the concept of local electricity sales and distribution are infeasible for car manufacturers. In addition, some owners of electric cars are of course interested in solar panels. It is no coincidence that Tesla bought the company SolarCity, which produces photovoltaic panels. So even this could be a very interesting new opportunity for dealers.

Say goodbye to your current business model

Thus, by 2030, a large part of car dealers will have to say goodbye to the existing business model and reorient themselves to the completely new operating conditions of the market. At the very least those selling Volvos. Most do not have the appropriate know-how or equipment to sell services, consulting, training, or especially electricity and photovoltaic panels. But a flexible and professional CRM system can easily help with this. For example, the cloud-based automotive CRM tool can perfectly cover existing sales, service, marketing, and customer car processes of the car dealer. However, thanks to its flexibility and cloud platform, it can quickly learn any other processes. Extending the existing CRM to the sale of services or other products is a breeze, especially when the company behind this system, Konica Minolta, has been supplying CRM systems in the fields of energy, including electricity distribution and sales, or service companies for years. And how are you prepared for Odessey 2030?

Sources

https://www.motor1.com/news/495958/vw-stopping-gas-engine-development/

https://www.cnbc.com/2021/03/05/vw-expects-half-of-us-sales-to-be-electric-vehicles-by-2030.html

https://www.bbc.com/news/business-56072019

The European car market is in decline, what to do now?

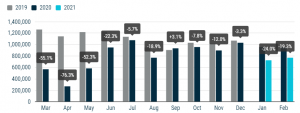

The European car market is in a sharp decline. According to data from the European Automobile Manufacturers Association (ACEA), year-on-year car sales fell by 24% in January and 19.3% in February. After a promising December, when the year-on-year decline was only 3.3%, this is a shock. What can you do as a dealer to maintain your sales performance?

The entire EU is in the same boat, with one exception

The drop in sales has affected all EU Member States. The largest year-on-year decreases were recorded in January and February in Lithuania (-46.5%), Portugal (-44.6%), and Denmark (-40.1%), with the smallest in Estonia (-8.8%), Finland (-8%), and Hungary (-6.8%). However, one and only country saw an increase in sales, and that was Sweden, by 12.8%. Sweden is known for its completely different approach to protecting its population from the coronavirus. This is the only significant difference from other EU Member States. Sweden has invested in maintaining normal life with some limited restrictions. Car sales have more than felt the positive effect of this policy.

Figure 1 – Source: ACEA

Other more sparsely populated countries in Europe are also holding steady

Outside the EU, there was another country that saw some growth, and that was neighboring Norway. There, sales increased by 5.4% year-on-year. Norway is unique in being the the only European country in the world to belong to the top 10 countries who best dealt with the coronavirus crisis, at least according to Bloomberg. In March, Norway had only 362 infections per 100,000 inhabitants, however, in all key metrics it did not differ much from the number 14 ranked Denmark, where car sales fell sharply.

However, the main driver for the increase in car sales is probably the enormous size of the country and the associated population density, which is the lowest in continental Europe (14 people per km2). Finland (16 people per km2), Sweden (23 people per km2), and Estonia (29 people per km2) are also not densely populated countries. In addition, Norway has long supported the sales of electric cars, which make up a considerable proportion of all cars sold. In contrast, neighboring Denmark, which has seen car sales fall sharply, has a relatively high population density (135 people per km2), which is similar to Portugal (112 people per km2). An exception, however is Lithuania (43 people per km2), where the state of the economy following coronavirus may play a role, as well as Hungary (105 people per km2), which is on the other side of the spectrum as the one of the few countries in Europe which closed its state borders.

What to do about declining sales

European market data clearly shows that declining sales affects the vast majority of European countries. It is due to both the economic recession and, apparently, a change in people’s habits. Where governments have implemented lockdowns, travel has simply decreased, and so has the need to buy new cars. Car dealerships in countries with higher population densities have a greater problem, where public transport is usually more accessible and there is less of a need for long journeys to work. While cars used to be sold widely and often according to similar rules and pan-European marketing campaigns, the COVID-19 pandemic has created massive differences between countries and groups. Presently, such widespread campaigns simply do not work anymore because in most European countries, only certain groups of population really need cars. What can be done about this?

Cars are sold only by those who know what customers need them

In order to continue selling, you need to know your customers in great detail. And you just have to be able to find them at the right time. It is obviously easier in Sweden than in Denmark. The examples of Sweden and Norway may also give dealers in other countries the hope that when life in a given country returns to normal, car sales will resume. Until then, however, it is necessary to incorporate all the appropriate marketing skills and corresponding tools. The key to success will be the extraction of current customer data, for example from the service center, but also from certain social networks.

Automotive CRM, a cloud CRM that can incorporate data from service, sales, e-mail, and phone contacts, as well as interactions from social media thanks to which it provides a perfect 360° view of each potential customer, can help you. It can then divide the customers into various groups, to which it can precisely target marketing campaigns. In short, it allows you to sell specific models that meet the specific needs that specific customer groups looking for new or even used cars may need. For example, families with newborns, families with a 3rd child, or companies and individuals whose current car has rising service costs and is likely at the end of its life.

Sources

https://www.bloomberg.com/graphics/covid-resilience-ranking/

https://en.wikipedia.org/wiki/Area_and_population_of_European_countries